3 Hacks for Calculating How Much Your Startup Needs to Raise

Many startups make fatal mistakes when calculating their financing needs. After running successful ventures, serving on boards of prominent startups, and advising hundreds of emerging entrepreneurs, HBS professors Shikhar Ghosh, Ramana Nanda, and William Sahlman observed common mistakes startups make when determining maximum financing needs. Here’s an overview of 3 essential things to help you figure out how much capital you need to raise to scale effectively, without getting overwhelmed by options and opinions, or swayed by offers.

3 Hacks for Calculating How Much You Need to Raise

- Map out your cumulative cash flow needs.

- Don’t let your desired valuation drive your approach. Think strategically.

- Don’t rely on “best” financial practices as you grow.

Understanding and applying each practice will help you gain a realistic idea of the amount of funding you need to scale.

Map Your Cumulative Cash Flow Needs

Map Your Cumulative Cash Flow Needs

Revenue growth and profitability are important, but without positive cash flow, a company cannot remain in control of its destiny. To determine how much you need to scale, you need to understand the importance of cash flow.

Free cash flow (FCF) is the amount of cash your company generates after paying all operating and capital expenses.

Your cash flow influences a range of issues, including your level of ownership and control over your company and it defines the risk VCs associate with your company. It’s common for founders to create a growth plan without considering the dynamics of cash flow and to underestimate the fluid relationship between cash flow and growth. Shikhar Ghosh, Professor of Business Administration at HBS, entrepreneur, and investor dubbed a “Master of the Internet Universe” by Forbes, observes,

“So many founders focus on the end goal—they want to grow their business. They don’t realize that growth can actually kill their company because without positive cash flow a company cannot remain in control of its destiny.”

Statistics support this statement. In 2017, over 70% of tech startups failed to exit or raise follow-on funding despite their growth. Almost everyone has heard that “cash is king”; what makes cash flow so widely misunderstood and easy to miscalculate?

The short answer: growth—especially rapid growth—diminishes cash flow and that shortage can create myriad unanticipated problems. What can you do to avoid this? Get familiar with your cumulative cash flow curve before seeking investment, understand the factors that drive cash flow, and develop a strong cash management plan that accounts for the growth’s impact on cash flow.

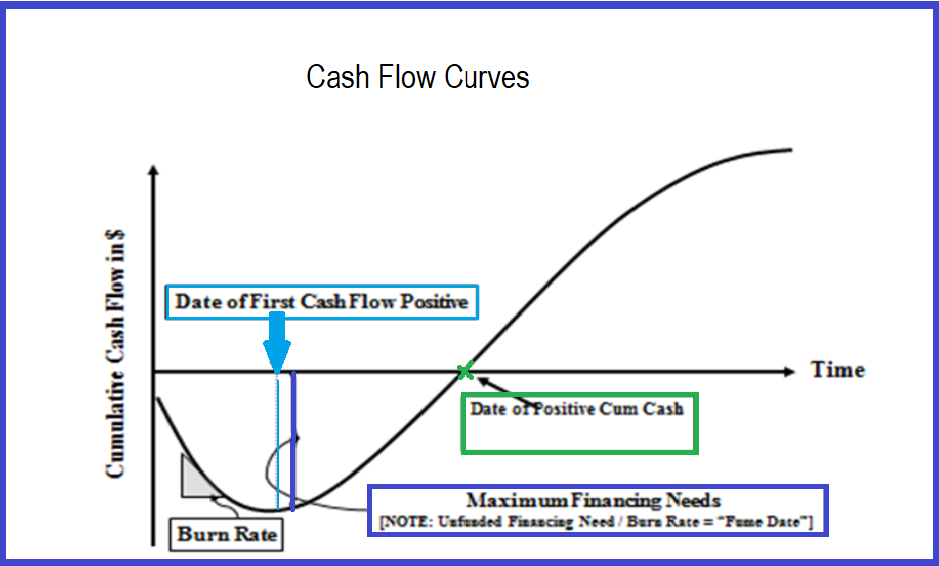

Cash Flow Curve

Cash flow incorporates items that go into the income statement, such as profit margin, and items that go into the balance sheet, such as changes in working capital required.

We can define free cash flow (FCF) as:

FCF = EBIAT – (CAPEX – DEPRECIATION) – Δ NET WORKING CAPITAL

In most early stage companies, the cash flow curve starts at zero. The rate at which cash declines as you use it is known as the burn rate. As your expenses continue to accrue, you burn through cash and hit the bottom of the curve. When the curve begins turns up, you start making a profit.

Don’t Count Projected Revenue as Available Cash

From a quantitative perspective, determining cash flow at a given point seems straightforward. But it’s surprisingly easy to overestimate your cash flow when determining maximum financing needs. Ghosh observes that “Many startups determine their funding needs by estimating the point at which revenue will arrive, then making plans based on that predicted revenue. But revenue often takes longer to arrive.” This invariably leads to cash flow shortages.

The unfunded time between your date of first cash flow positive and maximum financing needs is known as the fume date—an estimated point for when a business will deplete its cash and run on fumes until it collapses.

Factors to Consider When Calculating Finance Needs

- What is your overall net present value?

- What is the shape of your cash flow curve?

- How long it will take to reach positive cash flow? How deep will the trough plunge?

Don’t Let a Desired Valuation Drive Your Decision

Don’t Let a Desired Valuation Drive Your Decision

Often, the answer to “how much money should I raise?” becomes influenced by emotion, instead of strategic thinking. Some founders determine an amount and consider how investment affects their dilution, without mapping out cash flow. Ghosh notes this as a common but potentially fatal mistake.

“Many founders say, ‘I want to get 2 million dollars and I want to give up 40%.’ They assume they can get to the next round, but they haven’t done the calculations or seen the implications. Working in this way, most don’t make it.”

Shikhar Ghosh

If you seek a high valuation at the beginning, understand the consequences: receiving a large sum upfront will typically be deemed a higher risk, diluting your equity. Many founders opt to accept the trade-off because they’ve become attached to the idea of raising a certain amount.

Reduce Uncertainty and Risk in Stages

The problem is, it’s rare that one round of financing will meet most startup’s needs. A growing business encounters many variables—market changes, emerging competitors, and changes in customers’ tastes. Plus, unforeseen opportunities often arise so it’s nearly impossible to predict your needs with precision. Ramana Nanda, professor of business administration at HBS, summarizes, “Money is time. You must consider time and money simultaneously.”

Ask yourself, “how much time do I need to figure out my uncertainties? How much time do I need to prove my hypothesis?” Then, when you have that number, add a substantial buffer to buy yourself the time you need.

Calculating how much to raise in this manner, instead of striving to hit a particular number or valuation, increases your chances of succeeding as it forces you to think strategically and incorporate your business model into your fundraising plan. As William A. Sahlman, Professor of Business Administration at HBS summarizes,

“You raise money to buy time. You buy time to run experiments. You run experiments to reduce uncertainty. You reduce uncertainty to get more money.”

William A. Sahlman

Most founders receive funds in installments–after you reach agreed-upon milestones or inflection points. When you reach an inflection point without running out of cash, you prove your value and unlock another round of funding. Each time you meet an inflection point you minimize your dilution, decrease your risk to investors and the valuation of your company rises. That cycle repeats through subsequent funding rounds.

When you don’t have enough cash flow circulating and can’t reach an inflection point, you enter dangerous territory. You need to raise more funding just to stay alive. And raising a new round when you’re short on cash puts you in the precarious position of a down round.

Don’t rely on past behaviors or best financial practices as you scale

Don’t rely on past behaviors or best financial practices as you scale

As you scale, you may need to temporarily suspend some financial best practices. For instance, focusing on revenue growth, establishing assets, and long-term savings seems smart. Many people reasons that buying office space instead of renting may save money in the long run, because you’re investing in an asset. Many startups believe that, while acquiring a customer is expensive, over time, the customer will more than pay back the costs. But both rationales can be harmful from a cash flow perspective.

Assets Drain Cash Flow

Acquiring assets may be beneficial in the future, but assets compound cash flow. Similarly, high customer acquisition costs create low profitability in the short term, with the additional risk that your customer lifetime value may change or become lower than you estimated.

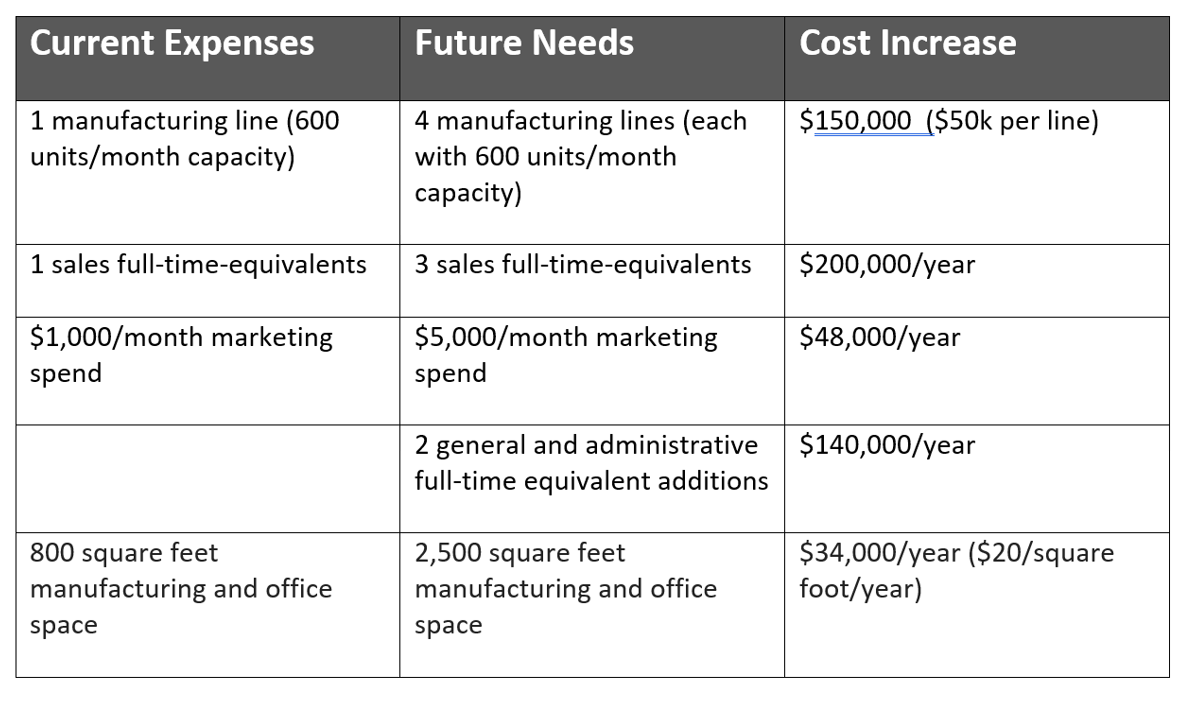

Imagine you own a company that makes cell phone covers with a built-in battery pack. Customers love the product design and sales have skyrocketed. You sell each cell phone case for $99 and generate $15 of profit per sale. You’ve reached manufacturing and sales capacity and the potential market size has expanded exponentially. You’re ready to scale. Your current profit won’t cover the rising expenses for manufacturing, sales, and overhead needed to grow, so you’re seeking funding, trying to determine how much to raise.

Using Your Current Model to Predict Growth Needs Will Backfire

At this stage, most founders use their current business and financial models to predict total funding needs, like this:

In this case, based on in-house manufacturing and sales capabilities, you predict cost increases to expand. This approach is common but short-sighted.

Key Mistakes

- Neglecting to build in room for unexpected expenses or spiraling costs.

- Not accounting for the likelihood of time overruns.

- Assuming that efficiency will increase in a neat linear fashion, in tandem with growth.

- Failing to consider cash flow in relation to other business decisions.

The strategies that worked to get the company to its current point might hinder it as it scales. For instance, outsourcing production at this point might lead to lower profitability; but it could also reduce cash flow deficit. Having more cash available could reduce total funding needs, enabling the founders to retain more ownership. Cash allows you to respond to unexpected obstacles or opportunities that arise.

Startups are affected by both external and internal forces. Choices that worked for a competitor may not work for your company because of your cash flow situation. Decisions that worked for you in the past may not work as you scale.

Your Questions & Answers